Disclosure: This post may contain affiliate links, meaning we get a commission if you decide to make a purchase through our links, at no cost to you. Please read our disclosure for more info.

If you're looking for a way to rebuild your credit, you may want to consider using a buy now pay later site like Perpay. These sites can be a great way to get started on rebuilding your credit history. You can use them to buy things that you need, and then pay off the balance over time. This can be a great way to get back on track financially.

Most Perpay stores will report your monthly payments to the credit bureaus, which can help to improve your credit score. You'll also have a set credit limit, which can help you to manage your finances and avoid getting into debt. And, if you make your payments on time each month, you'll be able to build up a good payment history, which is one of the most important factors in calculating your credit score.

So, if you're looking for a way to re-build your credit, perpay stores could be a great option for you.

image credit: Perpay.com

In This Post:

- What is Perpay?

- How does Perpay Credit Building Work?

- Does Perpay Have An App?

- Who is Perpay good for?

- What Perpay Store Brands Can I Buy?

- Is Perpay Safe?

- Perpay Referral Program

- Alternative Companies like Perpay

- Buy Now Pay Later Apps – Pay in 4 Alternatives to Perpay

- How to Apply with Perpay

- Is Perpay for you?

What is Perpay?

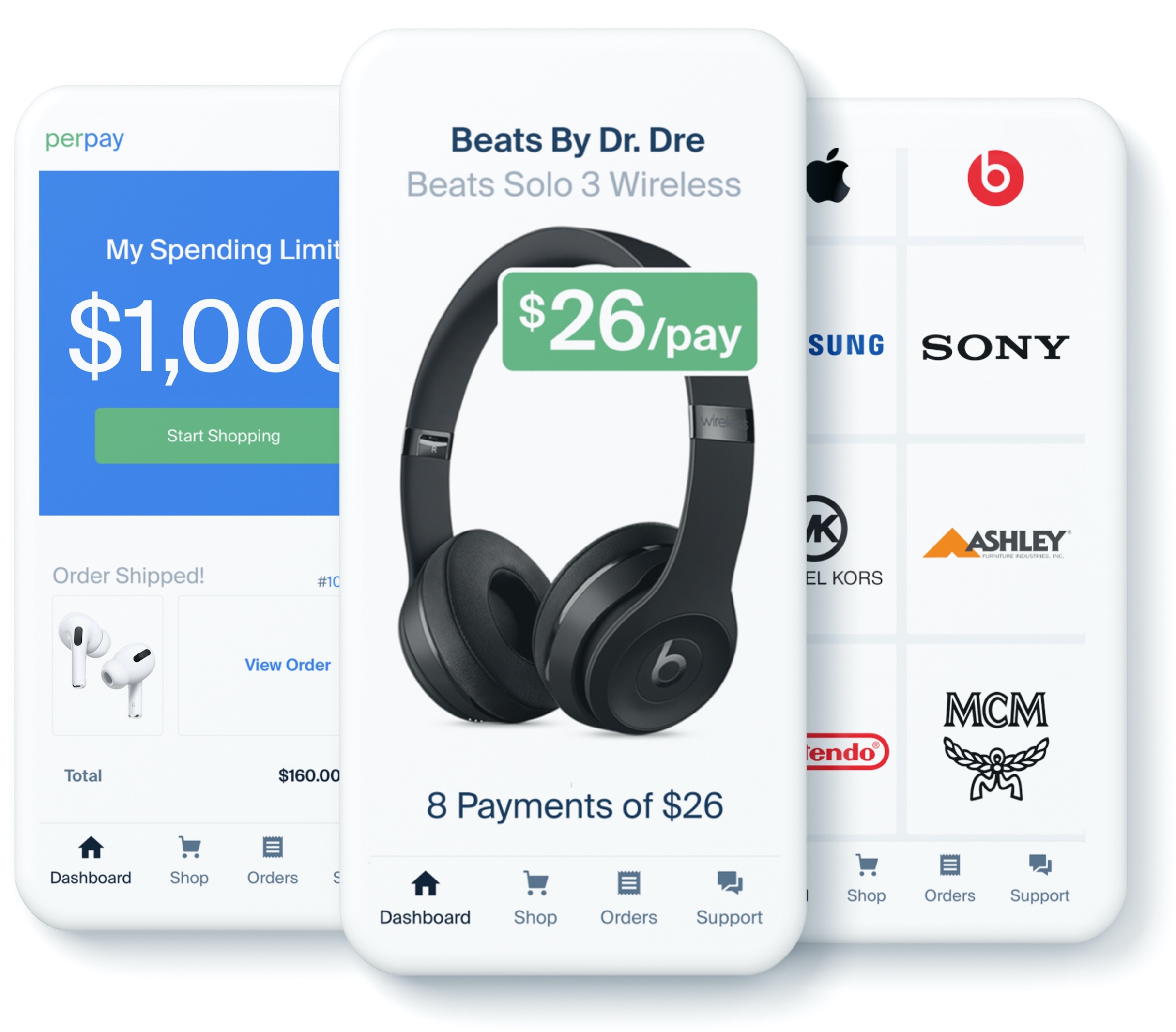

Perpay is a unique interest-free payment system that can help you improve or rebuild your credit score. How it works is simple – first, you get approved based on your monthly income. Perpay doesn't run a credit check, but instead verifies your employment and income, and then sets a credit limit based on your salary.

With this pre-approved credit limit, you can make online purchases from any participating store within your budget. You make small payments from your paycheck each month until the balance is paid off. As you make timely payments, Perpay reports your positive activity to the major credit bureaus, which can help to improve your credit score over time.

So not only can Perpay help you make everyday purchases more affordable, but it can also give you a boost in the world of credit. It's a win-win!

Perpay is the all-in-one shopping app that makes it easy to buy your favorite brands, pay over time, and build credit along the way.

With a spending limit of $1,000 and small payments taken directly from your paycheck, Perpay makes it easy to manage your finances and make purchases without having to worry about fees, interest, or credit checks.

Plus, with an average credit score increase of 39 points, you can rest assured that using Perpay will help you build your credit history.

So why wait? Join the Perpay community of 3+ million members today and start enjoying the convenience of interest-free shopping.

How does Perpay Credit Building Work?

Perpay is a unique credit-building service that allows you to pay for items over time, interest-free. With Perpay, you can build your credit score quickly and easily as long as you make your payments on time. Here's how it works:

First, you choose the items you want to purchase and pay for them using Perpay's pay cycle. Your first payment is typically due two weeks after you make your purchase, and subsequent payments are made via direct deposit from your paycheck.

As long as you make your payments on time, there is no interest charged on the balance. This makes it easy to pay off your balance and improve your credit score. You can see an average increase of 39 points in just four months!

Choosing your own pay cycle

When you sign up for Perpay, you'll choose your pay cycle (every 2 weeks or monthly) and your payments will be automatically withdrawn based on that schedule.

You also have the option to make extra payments if you want to pay off your balance early. If you're interested in building credit, you can opt to have your Perpay payments reported to the major credit bureaus.

A consistent payment track record will help to increase your credit score over time. Keep in mind that Perpay is not a traditional line of credit – there is no grace period and late payments will incur fees. However, as long as you make your minimum payment on time, you won't pay any interest. With Perpay, you can buy now and pay later – interest free!

Does Perpay Have An App?

Yes, Perpay does have apps on for both Apple and Android phones. To download the app go to the Perpay site and scroll down to find the app store you need – Download the Perpay App from the Apple App Store or Google Play Store.

App reviews of Perpay are positive with a 4.7 out of 5 on the Apple app review page.

Shopping can be expensive, especially when buying items all at once. This is where Perpay comes in – four interest-free payments make it easy and affordable for anyone to shop!

You can use Perpay at any store and online stores that offer Afterpay, and there are many stores to choose from (more about this later). While some people may be hesitant to try a new financial technology company, the reviews for Perpay are very positive.

Users on the Apple app review page have given Perpay a 4.7 out of 5. People appreciate the convenience and affordability that their buy now pay later offer without incurring fees and bad credit.

Whether you're buying a new outfit or investing in a new entertainment system, Perpay can help you get the things you want now and pay later.

Who is Perpay good for?

Perpay is a great option for people who want to shop while still establishing their credit. By performing a soft credit check, Perpay is able to help people build their credit scores while they shop. Best of all, there are no interest charges associated with Perpay credit cards. Instead, customers simply make a series of fixed payments over time.

The amount of the payments and the number of payments will be determined based on the total purchase price. The payments are automatically deducted from the customer's linked bank account, so there is no need to worry about missing a payment.

If you have a full-time job, a mobile device where the Perpay app is compatible, no bankruptcy history, and a checking account, then Perpay is a great option for you.

What Perpay Store Brands Can I Buy?

One thing to know about shopping with Perpay is that you have to purchase through the Perpay App in order to use the service. You cannot use Perpay at checkout at partner retailers. With that said, Perpay does partner with some of the biggest brands in Home, Electronics, Toys and Fashion. This means you can shop for Apple devices, Samsung phones, Michael Kors shoes, handbags and clothing, Nintendo Switch, Ashley Homestore sofas, bedroom sets and more!

However, it's important to keep in mind that Perpay prices for all these brand names are at a premium. This is because you are paying for the credit building service. So if you can afford to buy these items outright with cash or another Buy Now Pay Later service that has no fees, you will save money in the long run

Another thing to note is that Perpay has a much longer repayment period than other services. This means you could pay interest on your purchase for a long time. Plus, if you're late on a payment, there are late fees involved. So be sure to keep up with your payments!

Overall, Shopping with Perpay is a great way to get the items you want while building credit. Just be sure to factor in the extra cost of using the service and make sure you can keep up with your payments before making a purchase.

Is Perpay Safe?

Yes Perpay is legit, the products you receive are from the actual brand names. In order for your product to ship you do need to make the first payment via your payroll direct debit, this is the Perpay way of verifying income and employment.

The one thing to really be careful of with any credit building products from loans to credit cards and buy now pay later services is that you have steady cash flow from your job and that you are totally confident you can make the monthly payments.

Perpay does not charge late fees or additional penalties for late payments but they will send your non-payment status to the credit reporting agencies so if you don’t pay it will negatively impact your credit.

Perpay Referral Program

Perpay also offers a referral program where you can get up to $100 credit towards your first order.

Payday loans can be a lifesaver when you're short on cash and need to cover an unexpected expense before your next payday.

However, it can also be a pricey way to borrow money, and they can quickly become overwhelming if you're not careful. That's why Perpay offers a referral program, so you can get up to $100 credit towards your first order.

To take advantage of the referral program, simply refer your friends or family members to Perpay. For each person who signs up and is approved for a payday loan, you'll receive a $20 credit.

There's no limit to how many people you can refer, so you can potentially earn a significant amount of credit towards your future payments.

image credit: Perpay.com

Alternative Companies like Perpay

If you are looking for an alternative to Perpay, Acima is a great option. Like Perpay, Acima personalized spending limit and does not require a credit check. However, one key difference is that Acima does not require an upfront payment.

Instead, you will make weekly or bi-weekly payments until the balance is paid off. This makes it a great option if you are trying to build your credit. Another great alternative is The Horizon Outlet.

This site also offers a personalized spending limit and interest free payments, and does not require a credit check. However, one key difference is that The Horizon Outlet requires an upcoming payment in order to use the site.

This is great if you are trying to build your credit but need to make a purchase right away. Whichever option you choose, be sure to read the terms and conditions carefully so that you understand the requirements and can make the best decision for your needs.

Lease to Own – Build Credit Alternatives to Perpay

If you're looking for ways to build credit, but aren't sure Perpay is right for you? It's a popular option, but it's not the only one. There are several other ways to build credit that don't involve using Perpay. Below are alternatives so you can make an informed decision about what's best for you.

- Acima Credit – Lease to own and build credit

- The Horizon Outlet – Credit card designed for bad credit

- Progressive Leasing – find stores that offer this pay over time option

For the most cost effective alternatives try any of the major Buy Now Pay Later Apps that offer no credit check approvals:

Buy Now Pay Later Apps – Pay in 4 Alternatives to Perpay

If you're looking for a more cost-effective way to shop, try any of the major Buy Now Pay Later Apps that offer no credit check approvals.

These apps can be a great way to get the things you want without having to worry about payments right away. Plus, many of these apps have unique features that can make your shopping experience even better.

So, what are you waiting for? Start exploring these alternative Buy Now Pay Later Apps today!

- Afterpay – List of stores that accept Afterpay Buy Now Pay Later

- Abuda – Buy Now Pay Later for anything on Amazon

- Sezzle – List of retailers that offer Sezzle Buy Now Pay Later

- Klarna – Online stores that accept Klarna to Buy Now Pay Later

- Affirm – Online stores that accept Affirm Buy Now Pay Later

- Paypal Credit

- QuadPay – Online stores that accept QuadPay

- Shop Pay – Online stores that accept ShopPay by Shopify

How to Apply with Perpay

Applying for a loan with Perpay is a quick and easy process that can be completed entirely online. To get started, you'll need to provide some basic personal and financial information. This includes your income, which can be verified using a recent pay stub. Once you've finished filling out your profile, you'll be able to browse the market and add products to your cart.

You need can then submit your shopping cart for an assessment so that their system may provide you with approval and an individualized spending cap. Once you've been accepted, Perpay will contact you to provide information on how to make any future payments.

You'll have the option to make either weekly or bi-weekly payments, and there are no hidden fees or charges for early repayment. You can also choose how many installments you'd like to make, up to a maximum of 24.

Curious about other ways to shop without the hassle of a credit check? Cruise over to our companion article, “Buy Now Pay Later Sites with No Credit Check,” for a list of platforms that let you make purchases without the worry of a credit inquiry.

Is Perpay for you?

Perpay is a great option for those who want to shop and build their credit score simultaneously. It is beneficial if you're looking for an alternative to traditional credit card accounts, as it requires no high-interest charges or long-term commitment.

Plus, you can choose when to pay, giving you some freedom and flexibility with your payments. It also doesn't require a hard credit check, so it's perfect for those who are just starting to build their credit

However, Perpay may not be the best option for everyone. Its terms and conditions vary from state to state, so you'll need to make sure that it's available in your area before signing up.

Additionally, you must have a minimum income of $400 per week in order to qualify – this can be difficult for those who are self-employed or who only have part-time jobs.

Finally, you must have a bank account in order for Perpay to be able to withdraw your payments. If any of these criteria are difficult for you to meet, then another Buy Now Pay Later option might be more suitable.

We hope this article has helped introduce you to Perpay and the Buy Now Pay Later services they offer. Every person's financial situation is unique, so it's important that you choose a payment plan that best fits your needs. Good luck!

Kim is a personal finance expert with a Bachelor’s degree in Finance from the University of Illinois at Chicago. Kim enjoys helping people take charge of their personal finances and has been doing so with her freelance writing for 15 years. She loves helping people break down difficult personal finance topics, helping them make smart financial decisions that make them feel empowered.